The world has experienced horrific pandemics before COVID-19, but it’s certainly difficult to remember one with such rapid speed and severe consequences.

Casting our minds back to the beginning of 2020, nobody foresaw the impact COVID-19 would have on our health, economy and social networks. Docks, airports and borders closed overnight – bringing shipments, cargo and contracts to a standstill. UK based supply chain partners, OCI, quoted back in April:

Such action formed part of a series of unprecedented steps to alleviate some of the pressures on trade invoked by the crisis. What was unknown at the time was the duration that COVID-19 would span and how long term impacts would be felt – almost a year on – on trading routes and the necessary transport hubs around the world. As trade flows have begun to resume, regulations, limitations and extreme pricing fluctuations have dramatically impacted almost all supply chains globally.

As the Guardian reports, it still remains an enormous challenge to enable free trade and the necessary flow of personnel, whilst trying to suppress any risk of transmission. New Zealand has arguably been the flagship for coronavirus containment and elimination within their population, but outside risk from imports – which is an inherent factor given the requirements and reliance on globalisation by almost all nations – is still providing them with enormous challenges.

But what does this really mean for global economic growth?

International trade and investment are key elements for global economic growth. Both have been dangerously affected by the pandemic, with world trade across all sectors of the economy expecting to fall between 13 percent and 32 percent in 2020, The WTO Director General reports. The implications of such a contraction in growth, in tandem with the direct impacts from the virus itself, will likely have unpredictable and deep routed implications – paid for by generations to come.

Whilst our primary concern is to take necessary caution to protect our health in the immediate term, we must also take appropriate measures to support and facilitate trade and investment at both international and domestic levels to support the medium/long term. We must take all precautions to ensure that this health crisis does not lead us further into an economic downhill spiral.

Of course, trade and investment play a key role in the fight against the current pandemic itself with medicine, PPE, supplies and equipment being shipped around the world.

Oliver Chapman, CEO of OCI, a global supply chain partner which currently supports and ships a range of PPE to governments worldwide, said;

“OCI is proud to support and supply our customers with quality and efficiency, utilising our extensive network and expertise which has been built up and refined for more than 12 years.

COVID-19 has been catastrophic for many consumer facing industries such as tourism and travel, but international trade must continue to be supported by governments and sensible policy globally as in the 20th Century it is clearly a necessity, not a luxury.”

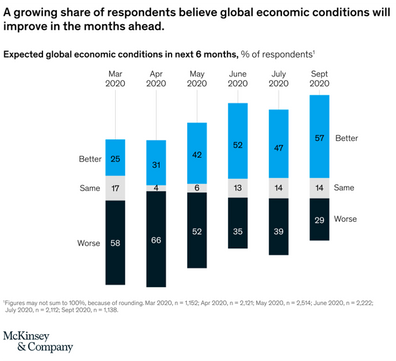

This graphic from McKinsey & Co. does however suggest a sense of optimism from a sample Executive for the global market conditions over the next 6 months. It’s clear from the above graphic and the sample surveyed, that as the pandemic has moved across nations over the last couple of quarters, economies have found a way to at least reemerge somewhat from their hibernation. This is likely to be factored in with, what is hoped, lower death rates due to better therapeutics, strategies around the virus and optimism of vaccines within the next 12 months. What is important to note is that post-September, many developed countries appear to be seeing a second wave and hence a subsequent survey may paint a different picture.

In the midst of significant uncertainty, there are four things we can do to support our economy via trade and investment:

1) Boost confidence in trade and global markets by improving transparency about trade-related policy actions and intentions;

2) Keep supply chains flowing, especially for essentials such as health supplies and food;

3) Avoid making things worse, through unnecessary export restrictions and other trade barriers;

4) Even in the midst of the crisis, think beyond the immediate. Government support today needs to be delivered in a way that ensures it serves the public interest, not vested or politically charged interests, and avoids becoming tomorrow’s market distortions.

OCI remains committed to sourcing, providing end to end logistics and flexible financing options in order to support partners worldwide and enable global trade. It is through this comprehensive solution that we are able to support large corporations and government entities with vital PPE requirements as they require it, even throughout the somewhat challenging global trade routes. For further information, please Contact Us.